This guide unravels common misconceptions about storm damage roof insurance, revealing what policies genuinely cover and the crucial areas often misunderstood. It’s essential reading for Atlanta homeowners navigating post-storm property issues, offering expert corrections to widespread beliefs and highlighting Dr. Roof’s role in simplifying your storm restoration and insurance claim process, ensuring you receive rightful coverage.

Unmasking the Truth: A Case for Full Coverage

When severe weather strikes the Atlanta metropolitan area, homeowners naturally look to their storm damage roof insurance for security. However, widespread confusion often surrounds what these policies truly protect.

Many assumptions can lead to unexpected out-of-pocket costs or even denied claims. This guide corrects common myths, offering clear evidence of what storm damage roof insurance genuinely covers and how to maximize your benefits.

The Hidden Cost of Misinformation for Homeowners

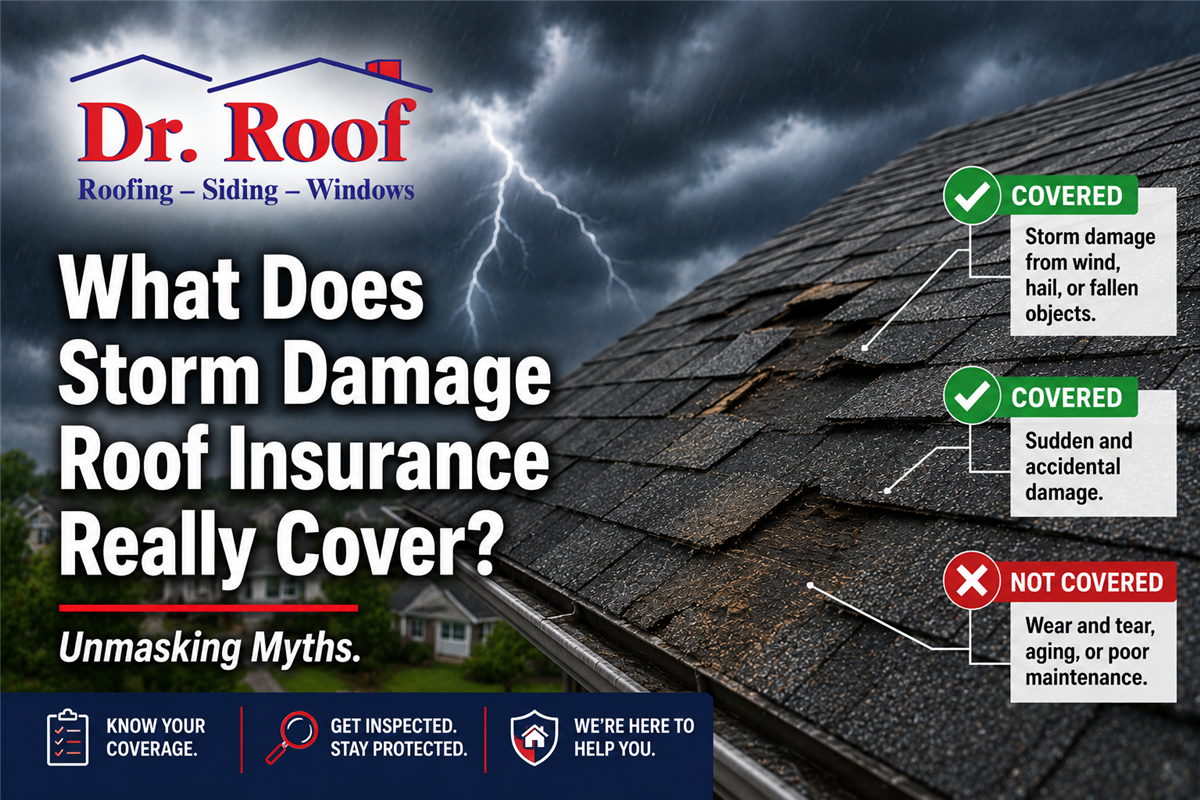

Homeowners frequently operate under several assumptions about their insurance policies that prove costly. It's a common misconception that all storm-related damage is automatically covered.

Insurance policies are complex, containing specific clauses on covered events and exclusions. Understanding these details is crucial for anyone facing post-storm repairs, as ignoring them can lead to significant financial surprises.

Common Myths That Jeopardize Your Storm Restoration Claim

One prevalent myth suggests that cosmetic damage, like minor hail dents not affecting roof function, is always covered. While some premium policies offer broader protection, standard storm damage roof insurance typically focuses on functional damage that compromises your roof’s integrity.

Another misunderstanding concerns damage reporting timelines. Many believe they can delay filing a claim until a leak appears. In reality, most policies require prompt notification, often within a year or even sooner, to prevent claims from being jeopardized by arguments of neglect.

The distinction between Actual Cash Value (ACV) and Replacement Cost Value (RCV) policies also confuses many homeowners. An ACV policy provides the depreciated value of your roof, whereas an RCV policy covers the cost of new materials without depreciation, offering superior protection for storm restoration.

We often encounter homeowners who believe their deductible applies uniformly. However, many policies include a separate, often higher, percentage-based deductible specifically for wind and hail damage. This means you might be responsible for a percentage of your home’s insured value before coverage begins, making policy review essential.

Finally, it's a mistake to assume you must accept the first offer from your insurance company. Initial settlement figures may not account for all necessary repairs. Having a qualified, GAF Master Elite certified contractor like Dr. Roof provide their own detailed assessment is invaluable in these situations.

Beyond Assumptions: Dr. Roof's Expert Advocacy

Many homeowners feel overwhelmed and unprepared to navigate the complex insurance claim process alone. However, qualified roofing contractors are highly experienced in working with insurance companies.

Our team at Dr. Roof provides comprehensive storm damage insurance assistance. We act as a crucial liaison, streamlining the process, ensuring all damage is properly documented, and advocating for your best interests. This support significantly reduces stress and improves claim outcomes.

Roswell Homeowner Secures Full Roof Replacement

In mid-2025, a client in Roswell experienced significant hail damage and initially received a low offer from their insurer. The homeowner, believing they had no other option, was prepared to accept less than full replacement cost.

Dr. Roof’s team intervened with a thorough, independent inspection. We identified subtle damage, including granule loss and compromised shingle seals, that the initial adjuster had missed. These issues would have led to future leaks.

We meticulously documented all findings, provided a comprehensive estimate, and advocated for the client during the re-inspection. Our efforts led to the client securing a full roof replacement, increasing their payout by over $12,000. The storm restoration was completed within five weeks of the revised claim approval.

A Strategic Partnership for Claim Success

Navigating a storm damage roof insurance claim effectively requires a methodical approach, especially when partnering with experts. Our process begins with an immediate, professional inspection after a storm.

Our GAF Master Elite certified team meticulously documents all damage, visible and hidden, providing irrefutable evidence. This detailed report, complete with photos and a precise estimate, provides a solid foundation for your claim.

We then assist clients in initiating their claim with their insurance provider, ensuring all necessary paperwork is correctly submitted and deadlines are met. This proactive step helps to avoid common pitfalls in the early stages of the claim.

A Dr. Roof project manager meets with your insurance adjuster on-site, highlighting all documented damage and discussing the full scope of storm restoration needed. This expert presence ensures no damage is overlooked.

We also help review the proposed settlement, cross-referencing it with our detailed estimate to ensure adequate coverage. If discrepancies arise, we assist in negotiating for a fair adjustment to secure sufficient funds for quality repairs.

Once the claim is approved and funding is secured, our experienced team proceeds with the highest quality storm restoration work. This is backed by our labor and material warranties, ensuring your roof is restored to superior, lasting condition.

Essential Lessons for Navigating Your Policy

It's vital to recognize that insurance policies typically cover new, sudden, and accidental damage directly caused by an insured peril. A common belief that any existing damage, even pre-dating a storm, will be covered is another myth.

Pre-existing wear, tear, or neglect are usually excluded. This underscores the critical importance of regular roof maintenance to prevent minor issues from escalating into major, uninsurable problems.

Protecting Your Home: Act with Knowledge and Partnership

Ultimately, understanding your storm damage roof insurance policy is paramount. Avoid relying on hearsay or assumptions; instead, take the time to read your policy documents and ask your insurance agent direct questions. Partnering with a reputable, experienced contractor is key to navigating the storm restoration process successfully.

Frequently Asked Questions

Is all storm-related roof damage automatically covered by my policy?

No, not all storm-related damage is automatically covered. Policies have specific clauses defining covered perils, and they often differentiate between functional damage and cosmetic issues. Pre-existing wear and tear or damage from events not listed in your policy are typically excluded, making a thorough policy review essential.

Will my insurance company instantly approve a claim for storm damage?

Instant approval for a storm damage roof insurance claim is not typical. The process involves an inspection by an adjuster, assessment of damage, and policy review. Professional contractors like Dr. Roof can provide detailed documentation to expedite this process and advocate on your behalf, but immediate approval is rare.

Do minor signs of storm damage truly warrant an insurance claim?

Yes, minor signs of storm damage can absolutely warrant an insurance claim, especially for effective storm restoration. It's crucial to get a professional inspection to identify all damage, visible or hidden.

Is it true that my deductible always applies in full to storm restoration?

Not always in the way many homeowners expect. While a deductible applies, some policies have specific, often higher, percentage-based deductibles for wind and hail damage, which are different from standard deductibles. It's critical to understand your policy's specific terms for storm damage roof insurance.

Can I simply accept the first insurance offer for storm damage without professional review?

It's generally not advisable to accept the first insurance offer without a professional review. The initial offer might not fully account for all damage or the complete scope of storm restoration needed. Having an experienced contractor like Dr. Roof provide an independent assessment ensures all necessary repairs are included and you receive fair compensation.

Subscribe to Dr. Roof's Blog

Comments